Anomaly Detection and Risk Early Warning System for Financial Time Series Based on the WaveLST-Trans Model

Article Information

Abstract

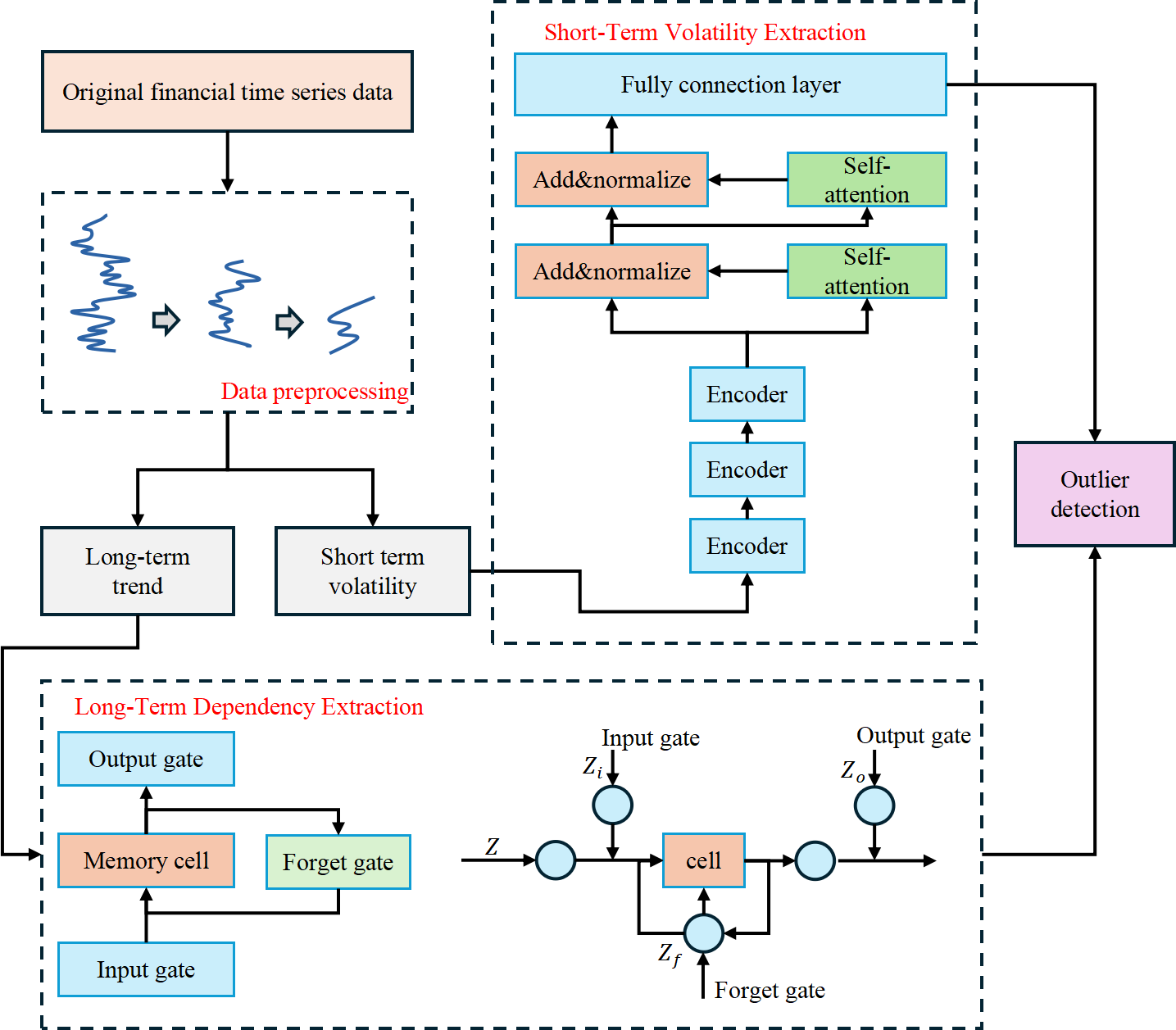

Abnormal fluctuations in financial markets may signal significant risks or market manipulation, so efficient time series anomaly detection methods are crucial for risk management. However, traditional statistical methods (e.g., ARIMA, GARCH) are difficult to adapt to the nonlinear and multi-scale characteristics of financial data, while single deep learning models (e.g., LSTM, Transformer) have limitations in capturing long-term trends and short-term fluctuations. In this paper, we propose WaveLST-Trans, a financial time series anomaly detection model based on the combination of wavelet transform (WT), LSTM and Transformer. The model first uses wavelet transform to perform multi-scale decomposition, extracts low-frequency trend and high-frequency fluctuation features, and feeds them into LSTM (to learn the long-term dependence) and Transformer (to capture local mutations) respectively, and finally integrates the multi-scale information through the feature fusion layer, which improves the detection accuracy and robustness. The experiments are conducted on Binance (cryptocurrency market) and S&P 500 (stock market) datasets, and the results show that WaveLST-Trans mostly outperforms the mainstream models in terms of F1-score, recall, and precision, and improves the detection performance by 3% and 10% in high-frequency market and long-term trend market, respectively. This study provides a more accurate and stable anomaly detection method for financial market risk management, which can be widely used in market regulation, quantitative trading and financial risk control, helping to improve the security and stability of the financial system.

Graphical Abstract

Keywords

Data Availability Statement

Funding

Conflicts of Interest

Ethical Approval and Consent to Participate

References

- Ahmed, M., Choudhury, N., & Uddin, S. (2017, July). Anomaly detection on big data in financial markets. In Proceedings of the 2017 IEEE/ACM International Conference on Advances in Social Networks Analysis and Mining 2017 (pp. 998-1001).

[CrossRef] [Google Scholar] - Chatzis, S. P., Siakoulis, V., Petropoulos, A., Stavroulakis, E., & Vlachogiannakis, N. (2018). Forecasting stock market crisis events using deep and statistical machine learning techniques. Expert systems with applications, 112, 353-371.

[CrossRef] [Google Scholar] - Fischer, T., & Krauss, C. (2018). Deep learning with long short-term memory networks for financial market predictions. European journal of operational research, 270(2), 654-669.

[CrossRef] [Google Scholar] - Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative finance, 1(2), 223.

[CrossRef] [Google Scholar] - Yıldız, K., Dedebek, S., Okay, F. Y., & Şimşek, M. U. (2022, September). Anomaly detection in financial data using deep learning: A comparative analysis. In 2022 Innovations in Intelligent Systems and Applications Conference (ASYU) (pp. 1-6). IEEE.

[CrossRef] [Google Scholar] - Alghofaili, Y., Albattah, A., & Rassam, M. A. (2020). A financial fraud detection model based on LSTM deep learning technique. Journal of Applied Security Research, 15(4), 498-516.

[CrossRef] [Google Scholar] - Mubalaike, A. M., & Adali, E. (2018, September). Deep learning approach for intelligent financial fraud detection system. In 2018 3rd International Conference on Computer Science and Engineering (UBMK) (pp. 598-603). IEEE.

[CrossRef] [Google Scholar] - Torres, J. F., Hadjout, D., Sebaa, A., Martínez-Álvarez, F., & Troncoso, A. (2021). Deep learning for time series forecasting: A survey. Big Data, 9(1), 3–21.

[CrossRef] [Google Scholar] - Vaswani, A., Shazeer, N., Parmar, N., Uszkoreit, J., Jones, L., Gomez, A. N., ... & Polosukhin, I. (2017). Attention is all you need. Advances in neural information processing systems, 30.

[Google Scholar] - Zhou, H., Zhang, S., Peng, J., Zhang, S., Li, J., Xiong, H., & Zhang, W. (2021, May). Informer: Beyond efficient transformer for long sequence time-series forecasting. In Proceedings of the AAAI conference on artificial intelligence (Vol. 35, No. 12, pp. 11106-11115).

[CrossRef] [Google Scholar] - Masini, R. P., Medeiros, M. C., & Mendes, E. F. (2023). Machine learning advances for time series forecasting. Journal of Economic Surveys, 37(1), 76–111.

[CrossRef] [Google Scholar] - Yu, H., Ming, L. J., Sumei, R., & Shuping, Z. (2020). A hybrid model for financial time series forecasting—integration of EWT, ARIMA with the improved ABC optimized ELM. IEEE Access, 8, 84501-84518.

[CrossRef] [Google Scholar] - Yang, T., Li, A., Xu, J., Su, G., & Wang, J. (2024). Deep learning model-driven financial risk prediction and analysis. Applied and Computational Engineering, 77, 196–202.

[CrossRef] [Google Scholar] - Guo, T., Zhang, T., Lim, E., Lopez-Benitez, M., Ma, F., & Yu, L. (2022). A review of wavelet analysis and its applications: Challenges and opportunities. IEEE Access, 10, 58869–58903.

[CrossRef] [Google Scholar] - Bao, W., Yue, J., & Rao, Y. (2017). A deep learning framework for financial time series using stacked autoencoders and long-short term memory. PloS one, 12(7), e0180944.

[CrossRef] [Google Scholar] - Wu, H. S. (2016, December). A survey of research on anomaly detection for time series. In 2016 13th international computer conference on wavelet active media technology and information processing (ICCWAMTIP) (pp. 426-431). IEEE.

[CrossRef] [Google Scholar] - Blázquez-García, A., Conde, A., Mori, U., & Lozano, J. A. (2021). A review on outlier/anomaly detection in time series data. ACM computing surveys (CSUR), 54(3), 1-33.

[CrossRef] [Google Scholar] - Xu, H., Pang, G., Wang, Y., & Wang, Y. (2023). Deep isolation forest for anomaly detection. IEEE Transactions on Knowledge and Data Engineering, 35(12), 12591–12604.

[CrossRef] [Google Scholar] - Samariya, D., & Thakkar, A. (2023). A comprehensive survey of anomaly detection algorithms. Annals of Data Science, 10(3), 829–850.

[CrossRef] [Google Scholar] - Qiao, Y., Wu, K., & Jin, P. (2021). Efficient anomaly detection for high-dimensional sensing data with one-class support vector machine. IEEE Transactions on Knowledge and Data Engineering, 35(1), 404–417.

[CrossRef] [Google Scholar] - Tang, Q., Fan, T., Shi, R., Huang, J., & Ma, Y. (2021). Prediction of financial time series using LSTM and data denoising methods. arXiv preprint arXiv:2103.03505.

[CrossRef] [Google Scholar] - Reddy, N. M., Sharada, K. A., Pilli, D., Paranthaman, R. N., Reddy, K. S., & Chauhan, A. (2023, June). CNN-Bidirectional LSTM based Approach for Financial Fraud Detection and Prevention System. In 2023 International Conference on Sustainable Computing and Smart Systems (ICSCSS) (pp. 541-546). IEEE.

[CrossRef] [Google Scholar] - Xu, J., Wu, H., Wang, J., & Long, M. (2021). Anomaly transformer: Time series anomaly detection with association discrepancy. arXiv preprint arXiv:2110.02642.

[CrossRef] [Google Scholar] - Karim, F., Majumdar, S., Darabi, H., & Chen, S. (2017). LSTM fully convolutional networks for time series classification. IEEE Access, 6, 1662-1669.

[CrossRef] [Google Scholar] - Ma, X., Wu, J., Xue, S., Yang, J., Zhou, C., Sheng, Q. Z., ... & Akoglu, L. (2021). A comprehensive survey on graph anomaly detection with deep learning. IEEE Transactions on Knowledge and Data Engineering, 35(12), 12012–12038.

[CrossRef] [Google Scholar] - Wu, D., Wang, X., & Wu, S. (2022). A hybrid framework based on extreme learning machine, discrete wavelet transform, and autoencoder with feature penalty for stock prediction. Expert Systems with Applications, 207, 118006.

[CrossRef] [Google Scholar] - Li, J., Liu, Y., Gong, H., & Huang, X. (2024). Stock price series forecasting using multi-scale modeling with boruta feature selection and adaptive denoising. Applied Soft Computing, 154, 111365.

[CrossRef] [Google Scholar] - Shih, S. Y., Sun, F. K., & Lee, H. Y. (2019). Temporal pattern attention for multivariate time series forecasting. Machine Learning, 108, 1421-1441.

[CrossRef] [Google Scholar] - Binance. (2024). Binance API documentation: Market data endpoints. Binance Developer Portal. Retrieved from https://developers.binance.com/docs/binance-spot-api-docs

[Google Scholar] - Yahoo Finance. (2024). S&P 500 historical data. Yahoo Finance Market Data. Retrieved from https://finance.yahoo.com/quote/%5EGSPC/history/

[Google Scholar] - Lim, B., Arık, S. Ö., Loeff, N., & Pfister, T. (2021). Temporal fusion transformers for interpretable multi-horizon time series forecasting. International Journal of Forecasting, 37(4), 1748–1764.

[CrossRef] [Google Scholar] - Audibert, J., Michiardi, P., Guyard, F., Marti, S., & Zuluaga, M. A. (2020, August). Usad: Unsupervised anomaly detection on multivariate time series. In Proceedings of the 26th ACM SIGKDD international conference on knowledge discovery & data mining (pp. 3395-3404).

[CrossRef] [Google Scholar] - Deng, A., & Hooi, B. (2021, May). Graph neural network-based anomaly detection in multivariate time series. In Proceedings of the AAAI conference on artificial intelligence (Vol. 35, No. 5, pp. 4027-4035).

[CrossRef] [Google Scholar] - Yue, Z., Wang, Y., Duan, J., Yang, T., Huang, C., Tong, Y., & Xu, B. (2022, June). Ts2vec: Towards universal representation of time series. In Proceedings of the AAAI conference on artificial intelligence (Vol. 36, No. 8, pp. 8980-8987).

[CrossRef] [Google Scholar] - Munir, M., Siddiqui, S. A., Dengel, A., & Ahmed, S. (2018). DeepAnT: A deep learning approach for unsupervised anomaly detection in time series. IEEE access, 7, 1991-2005.

[CrossRef] [Google Scholar]

Cited By (3)

-

Xinyi Liang, Ruizhe Zhou, Yinghao Zhao, Kewei Cao, Mingfan Chang, Yihan Zheng. .

Proceedings of the 2026 International Conference on Generative Artificial Intelligence and Education, 2026 .

[CrossRef] -

Haiying Cao. Interpretable financial time series anomaly detection based on frequency domain features and enhanced sparse attention.

Applied Intelligence, 2026 , 56 (10).

[CrossRef] -

Yue Yang, Zihan Su, Ying Zhang, Chang Chuan Goh, Yuxiang Lin, Anthony Graham Bellotti, Boon Giin Lee. Kolmogorov–Arnold networks-based GRU and LSTM for loan default early prediction.

Applied Soft Computing, 2026 , 197 .

[CrossRef]

Cite This Article

TY - JOUR AU - Su, Tian AU - Li, Runlong AU - Liu, Bo AU - Liang, Xiaoxiang AU - Yang, Xinhao AU - Zhou, Yan PY - 2025 DA - 2025/05/21 TI - Anomaly Detection and Risk Early Warning System for Financial Time Series Based on the WaveLST-Trans Model JO - ICCK Transactions on Emerging Topics in Artificial Intelligence T2 - ICCK Transactions on Emerging Topics in Artificial Intelligence JF - ICCK Transactions on Emerging Topics in Artificial Intelligence VL - 2 IS - 2 SP - 68 EP - 80 DO - 10.62762/TETAI.2025.191759 UR - https://www.icck.org/article/abs/TETAI.2025.191759 KW - financial anomaly KW - anomaly detection KW - LSTM KW - transformer KW - wavelet transform AB - Abnormal fluctuations in financial markets may signal significant risks or market manipulation, so efficient time series anomaly detection methods are crucial for risk management. However, traditional statistical methods (e.g., ARIMA, GARCH) are difficult to adapt to the nonlinear and multi-scale characteristics of financial data, while single deep learning models (e.g., LSTM, Transformer) have limitations in capturing long-term trends and short-term fluctuations. In this paper, we propose WaveLST-Trans, a financial time series anomaly detection model based on the combination of wavelet transform (WT), LSTM and Transformer. The model first uses wavelet transform to perform multi-scale decomposition, extracts low-frequency trend and high-frequency fluctuation features, and feeds them into LSTM (to learn the long-term dependence) and Transformer (to capture local mutations) respectively, and finally integrates the multi-scale information through the feature fusion layer, which improves the detection accuracy and robustness. The experiments are conducted on Binance (cryptocurrency market) and S&P 500 (stock market) datasets, and the results show that WaveLST-Trans mostly outperforms the mainstream models in terms of F1-score, recall, and precision, and improves the detection performance by 3% and 10% in high-frequency market and long-term trend market, respectively. This study provides a more accurate and stable anomaly detection method for financial market risk management, which can be widely used in market regulation, quantitative trading and financial risk control, helping to improve the security and stability of the financial system. SN - 3068-6652 PB - Institute of Central Computation and Knowledge LA - English ER -

@article{Su2025Anomaly,

author = {Tian Su and Runlong Li and Bo Liu and Xiaoxiang Liang and Xinhao Yang and Yan Zhou},

title = {Anomaly Detection and Risk Early Warning System for Financial Time Series Based on the WaveLST-Trans Model},

journal = {ICCK Transactions on Emerging Topics in Artificial Intelligence},

year = {2025},

volume = {2},

number = {2},

pages = {68-80},

doi = {10.62762/TETAI.2025.191759},

url = {https://www.icck.org/article/abs/TETAI.2025.191759},

abstract = {Abnormal fluctuations in financial markets may signal significant risks or market manipulation, so efficient time series anomaly detection methods are crucial for risk management. However, traditional statistical methods (e.g., ARIMA, GARCH) are difficult to adapt to the nonlinear and multi-scale characteristics of financial data, while single deep learning models (e.g., LSTM, Transformer) have limitations in capturing long-term trends and short-term fluctuations. In this paper, we propose WaveLST-Trans, a financial time series anomaly detection model based on the combination of wavelet transform (WT), LSTM and Transformer. The model first uses wavelet transform to perform multi-scale decomposition, extracts low-frequency trend and high-frequency fluctuation features, and feeds them into LSTM (to learn the long-term dependence) and Transformer (to capture local mutations) respectively, and finally integrates the multi-scale information through the feature fusion layer, which improves the detection accuracy and robustness. The experiments are conducted on Binance (cryptocurrency market) and S\&P 500 (stock market) datasets, and the results show that WaveLST-Trans mostly outperforms the mainstream models in terms of F1-score, recall, and precision, and improves the detection performance by 3\% and 10\% in high-frequency market and long-term trend market, respectively. This study provides a more accurate and stable anomaly detection method for financial market risk management, which can be widely used in market regulation, quantitative trading and financial risk control, helping to improve the security and stability of the financial system.},

keywords = {financial anomaly, anomaly detection, LSTM, transformer, wavelet transform},

issn = {3068-6652},

publisher = {Institute of Central Computation and Knowledge}

}

Publisher's Note

ICCK stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and Permissions

Copyright © 2025 by the Author(s). Published by Institute of Central Computation and Knowledge. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made.

Copyright © 2025 by the Author(s). Published by Institute of Central Computation and Knowledge. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made.

Portico