An Analysis of Time Series Models for Predicting Global Rice Price

Article Information

Abstract

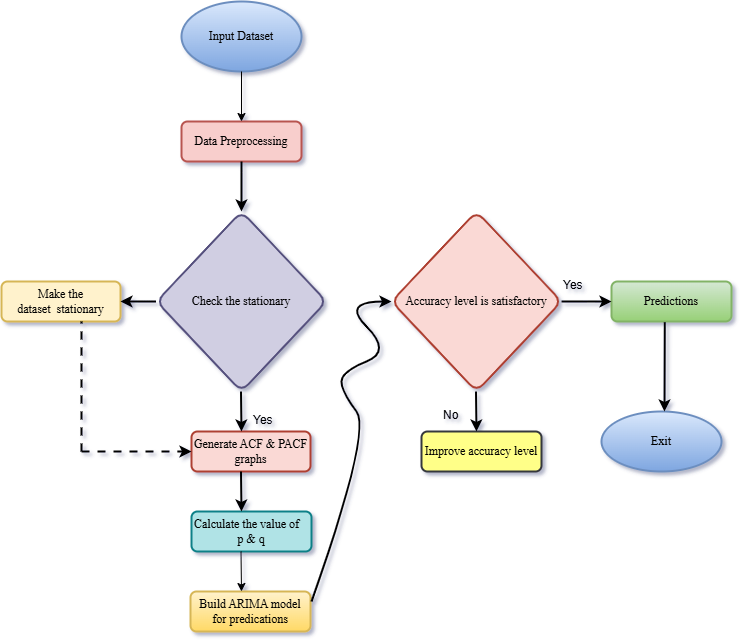

Rice plays a crucial role globally, as it is widely consumed across nations. Therefore, studying rice prices is vital, since fluctuations in the price can affect both its consumption and availability. This study analyzes time-series models using an international dataset. After preprocessing, the dataset comprises 71,856 samples and eight input features from six countries. The original dataset contained 300,816 rows and 23 columns. This study aims to predict rice inflation rates using time series models such as ARIMA, LSTM, and BiLSTM. The ARIMA model achieved the best combination of values (4,1,4)(0,0,0). Various statistical techniques that calculate inflation rates require expert knowledge and are time-consuming. However, with the advancement of intelligent computing and machine learning models, the rice inflation rate can now be predicted efficiently. These models play a vital role in managing unjustified surges in global rice prices.

Graphical Abstract

Keywords

Data Availability Statement

Funding

Conflicts of Interest

AI Use Statement

Ethical Approval and Consent to Participate

References

- Setivani, L., Handayani, H. H., & Geraldine, W. A. (2023, November). Rice Price Forecasting Using GridSearchCVand LSTM. In 2023 International Conference on Modeling & E-Information Research, Artificial Learning and Digital Applications (ICMERALDA) (pp. 127-131). IEEE.

[CrossRef] [Google Scholar] - Reddy, P. C. S., Suryanarayana, G. L. P. K., & Yadala, S. (2022, November). Data analytics in farming: rice price prediction in Andhra Pradesh. In 2022 5th International Conference on Multimedia, Signal Processing and Communication Technologies (IMPACT) (pp. 1-5). IEEE.

[CrossRef] [Google Scholar] - Yusri, N. H. M., Shafie, N. A., & Ghani, N. A. M. (2022, November). Rice price prediction in Malaysia. In 2022 IEEE International Conference on Computing (ICOCO) (pp. 249-252). IEEE.

[CrossRef] [Google Scholar] - Bilal, M., Alrasheedi, M. A., Aamir, M., Abdullah, S., Norrulashikin, S. M., & Rezaiy, R. (2024). Enhanced forecasting of rice price and production in Malaysia using novel multivariate fuzzy time series models. Scientific Reports, 14(1), 29903.

[CrossRef] [Google Scholar] - Duyapat, C. (2025). Forecasting Philippine Rice Prices: Comparison of Traditional Time Series and Machine Learning Models. Journal of Mathematics and Statistics Studies, 6(6), 18-28.

[CrossRef] [Google Scholar] - Zaw, T., Oo, A. N., & Kyaw, S. S. (2020, November). Combination of ARMA and BPNN model to predict rice type and rice price. In 2020 International Conference on Advanced Information Technologies (ICAIT) (pp. 159-164). IEEE.

[CrossRef] [Google Scholar] - Yusup, M., Prasetyo, S. Y. J., & Wellem, T. (2024, August). Evaluation of prediction accuracy in ARIMA and LSTM algorithms for agricultural commodity prices. In 2024 3rd International Conference on Creative Communication and Innovative Technology (ICCIT) (pp. 1-7). IEEE.

[CrossRef] [Google Scholar] - Haerani, E., Aulia, S. D., Darmawan, I., Rahmatulloh, A., Rizal, R., & Gunawan, R. (2025, February). Predicting the future: Using AdaBoost to forecast food commodity prices across Indonesian markets. In 2025 International Conference on Advancement in Data Science, E-learning and Information System (ICADEIS) (pp. 1-5). IEEE.

[CrossRef] [Google Scholar] - Phan, H., Nguyen, V., Vo, V., Tran, N. Q., Tran, L., Dao, S., & Pham, H. (2024, December). Leveraging automatically optimized forecasters and large language model for predicting Vietnamese rice export price. In 2024 RIVF International Conference on Computing and Communication Technologies (RIVF) (pp. 237-241). IEEE.

[CrossRef] [Google Scholar] - Mahawan, A., Jaiteang, S., Srijiranon, K., & Eiamkanitchat, N. (2022, February). Hybrid ARIMAX and LSTM model to predict rice export price in Thailand. In 2022 International Conference on Cybernetics and Innovations (ICCI) (pp. 1-6). IEEE.

[CrossRef] [Google Scholar] - Zhang, G. P. (2003). Time series forecasting using a hybrid ARIMA and neural network model. Neurocomputing, 50, 159-175.

[CrossRef] [Google Scholar] - Bhardwaj, S. P., Paul, R. K., Singh, D. R., & Singh, K. N. (2014). An Empirical Investigation of Arima and Garch Models in Agricultural Price Forecasting. Economic Affairs, 59(3), 415-428. http://dx.doi.org/10.5958/0976-4666.2014.00009.6

[Google Scholar] - Peng, Y. H., Hsu, C. S., & Huang, P. C. (2015, November). Developing crop price forecasting service using open data from Taiwan markets. In 2015 Conference on Technologies and Applications of Artificial Intelligence (TAAI) (pp. 172-175). IEEE.

[CrossRef] [Google Scholar] - Paul, R. K., Rana, S., & Saxena, R. (2016). Effectiveness of price forecasting techniques for capturing asymmetric volatility for onion in selected markets of Delhi. The Indian Journal of Agricultural Sciences, 86(3), 303-309.

[Google Scholar] - Darekar, A., & Reddy, A. A. (2017). Predicting market price of soybean in major India studies through ARIMA model. Journal of Food Legumes, 30(2), 73-76.

[CrossRef] [Google Scholar] - Anjoy, P., Paul, R. K., Sinha, K., Paul, A. K., & Ray, M. (2017). A hybrid wavelet based neural networks model for predicting monthly WPI of pulses in India. Indian J Agric Sci, 87(6), 834-839.

[Google Scholar] - Agarwal, P., Singh, R., & Singh, O. P. (2018). Dynamics of prices and arrivals of major vegetables: a case of Haldwani and Dehradun markets, Uttarakhand. Journal of Agricultural Development and Policy, 28(1), 1-11.

[Google Scholar] - Pandit, P., Sagar, A., Ghose, B., Dey, P., Paul, M., Alqadhi, S., ... & Abdo, H. G. (2023). Hybrid time series models with exogenous variable for improved yield forecasting of major Rabi crops in India. Scientific Reports, 13(1), 22240.

[CrossRef] [Google Scholar] - Choudhary, K., Jha, G. K., Das, P., & Chaturvedi, K. K. (2019). Forecasting potato price using ensemble artificial neural networks. Indian Journal of Extension Education, 55(1), 73-77.

[Google Scholar] - Bawa, M. U., Dikko, H. G., Shabri, A., Garba, J., & Sadiku, S. (2021). Forecasting performance of hybrid ARIMA-FIGARCH model and hybrid of ARIMA-GARCH model: a comparative study. Journal of Mathematical Problems, Equations and Statistics, 2(2), 48-58.

[Google Scholar] - Purohit, S. K., Panigrahi, S., Sethy, P. K., & Behera, S. K. (2021). Time series forecasting of price of agricultural products using hybrid methods. Applied Artificial Intelligence, 35(15), 1388-1406.

[CrossRef] [Google Scholar] - Paul, R. K., Yeasin, M., & Paul, A. K. (2022). The volatility spillover of potato prices in different markets of India. Current Science (00113891), 123(3).

[CrossRef] [Google Scholar] - Ajmal, S., Rohith, S., Unniravisankar, P., & Nabay, O. (2024). Price dynamics of tomato, onion and potato (TOP) in India. Asian Journal of Agricultural Extension, Economics & Sociology, 42(3), 134-143.

[CrossRef] [Google Scholar]

Cite This Article

TY - JOUR AU - Arya, Suraj AU - Kasana, Singara Singh PY - 2026 DA - 2026/03/23 TI - An Analysis of Time Series Models for Predicting Global Rice Price JO - ICCK Transactions on Machine Intelligence T2 - ICCK Transactions on Machine Intelligence JF - ICCK Transactions on Machine Intelligence VL - 2 IS - 3 SP - 116 EP - 126 DO - 10.62762/TMI.2025.272892 UR - https://www.icck.org/article/abs/TMI.2025.272892 KW - machine learning KW - time series analysis KW - global rice price prediction KW - ARIMA KW - LSTM KW - BiLSTM AB - Rice plays a crucial role globally, as it is widely consumed across nations. Therefore, studying rice prices is vital, since fluctuations in the price can affect both its consumption and availability. This study analyzes time-series models using an international dataset. After preprocessing, the dataset comprises 71,856 samples and eight input features from six countries. The original dataset contained 300,816 rows and 23 columns. This study aims to predict rice inflation rates using time series models such as ARIMA, LSTM, and BiLSTM. The ARIMA model achieved the best combination of values (4,1,4)(0,0,0). Various statistical techniques that calculate inflation rates require expert knowledge and are time-consuming. However, with the advancement of intelligent computing and machine learning models, the rice inflation rate can now be predicted efficiently. These models play a vital role in managing unjustified surges in global rice prices. SN - 3068-7403 PB - Institute of Central Computation and Knowledge LA - English ER -

@article{Arya2026An,

author = {Suraj Arya and Singara Singh Kasana},

title = {An Analysis of Time Series Models for Predicting Global Rice Price},

journal = {ICCK Transactions on Machine Intelligence},

year = {2026},

volume = {2},

number = {3},

pages = {116-126},

doi = {10.62762/TMI.2025.272892},

url = {https://www.icck.org/article/abs/TMI.2025.272892},

abstract = {Rice plays a crucial role globally, as it is widely consumed across nations. Therefore, studying rice prices is vital, since fluctuations in the price can affect both its consumption and availability. This study analyzes time-series models using an international dataset. After preprocessing, the dataset comprises 71,856 samples and eight input features from six countries. The original dataset contained 300,816 rows and 23 columns. This study aims to predict rice inflation rates using time series models such as ARIMA, LSTM, and BiLSTM. The ARIMA model achieved the best combination of values (4,1,4)(0,0,0). Various statistical techniques that calculate inflation rates require expert knowledge and are time-consuming. However, with the advancement of intelligent computing and machine learning models, the rice inflation rate can now be predicted efficiently. These models play a vital role in managing unjustified surges in global rice prices.},

keywords = {machine learning, time series analysis, global rice price prediction, ARIMA, LSTM, BiLSTM},

issn = {3068-7403},

publisher = {Institute of Central Computation and Knowledge}

}

Article Metrics

Publisher's Note

ICCK stays neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and Permissions

Portico